PBGC Update 2026: New Guarantees for Your Retirement

The Pension Benefit Guaranty Corporation (PBGC) Update 2026 introduces significant new guarantees designed to bolster retirement security for millions of Americans, ensuring defined benefit plans remain protected against insolvency and economic shifts.

Understanding the

The Evolving Role of the PBGC in 2026

The Pension Benefit Guaranty Corporation (PBGC) has long served as a vital safety net for American workers and retirees, protecting the pension benefits of over 31 million people in defined benefit plans. In 2026, its role has evolved, adapting to new economic realities and demographic shifts. These updates reflect a proactive approach to ensuring the stability of the pension system.

The PBGC’s mission remains steadfast: to protect the retirement incomes of American workers. However, the mechanisms and scope of that protection are continually refined. The 2026 updates are particularly noteworthy because they address long-standing concerns about benefit adequacy and the financial health of multiemployer plans, which have historically faced greater volatility. This strategic recalibration aims to fortify the system for decades to come, offering peace of mind to millions.

Historical Context and Recent Challenges

Historically, the PBGC has stepped in when private-sector defined benefit pension plans fail. This involves taking over the plan, becoming the trustee, and paying benefits up to statutory limits. Recent years have seen increased pressures on both single-employer and multiemployer plans due to market fluctuations, demographic changes, and the lingering effects of global economic events.

- Economic downturns impacting plan assets.

- Aging workforce leading to higher benefit payouts.

- Underfunded plans struggling to meet obligations.

- Legislative efforts to shore up the multiemployer program.

The challenges have necessitated a comprehensive review of the PBGC’s operational framework and guarantee levels. The 2026 updates are a direct response to these pressures, aiming to create a more resilient and equitable system for all beneficiaries.

In essence, the PBGC’s evolving role in 2026 is about more than just maintaining the status quo; it’s about strengthening the foundation of retirement security. These changes are designed to not only react to plan failures but also to proactively mitigate risks, ensuring that promised benefits are indeed delivered.

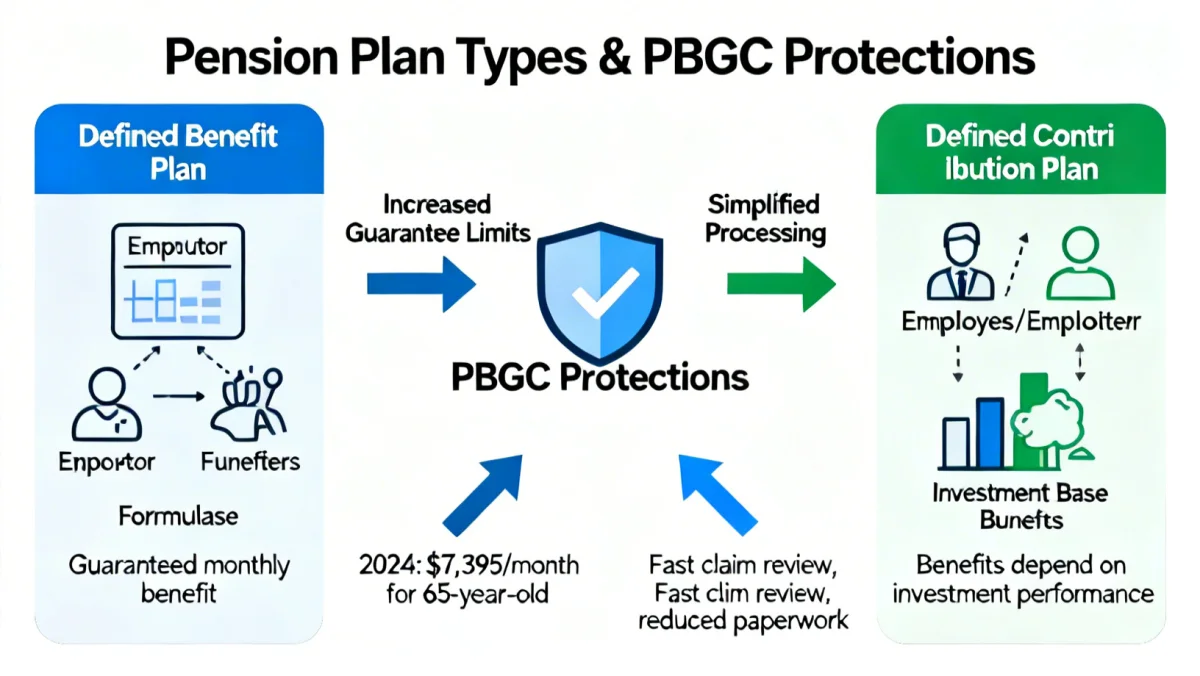

Understanding the New Guarantee Levels and Limits

The core of the PBGC Update 2026 lies in its revised guarantee levels and limits. These adjustments are critical for beneficiaries to understand, as they directly determine the maximum amount of pension benefit the PBGC will pay if a plan terminates or becomes insolvent. The changes aim to provide a more realistic and substantial level of protection.

For single-employer plans, the guarantee limits are typically adjusted annually based on inflation and other economic factors. However, the 2026 updates introduce specific enhancements beyond routine adjustments, particularly focusing on how these limits apply to different benefit structures. For multiemployer plans, which have historically had lower guarantee levels, the increases are even more significant, reflecting a commitment to equalize protection across various plan types.

Impact on Single-Employer Plans

For individuals in single-employer plans, the new guarantee limits mean a potentially higher safety net. The PBGC guarantees a certain monthly benefit, which varies based on your age at the time of plan termination and the form of benefit you choose. The 2026 changes often translate to a more robust guarantee, especially for those with long service records and higher pre-termination benefits.

- Higher monthly maximums for guaranteed benefits.

- Adjustments for early retirement benefits.

- Improved coverage for disability benefits.

It’s important to note that the guarantee limits are not a boundless promise. They cap the amount the PBGC will pay. However, the 2026 adjustments mean fewer individuals will hit this cap, ensuring a larger percentage of their earned benefits are protected.

Significant Boost for Multiemployer Plans

The most transformative changes in the PBGC Update 2026 are observed in the multiemployer program. Recognizing the unique vulnerabilities of these plans, the new guarantees significantly increase the protected benefit amounts. This move is a direct result of legislative actions and a concerted effort to prevent the severe benefit cuts that many multiemployer plan participants faced in the past.

These enhanced guarantees provide a much-needed lifeline for millions of workers and retirees in industries like construction, trucking, and retail, who rely on multiemployer pensions. The increased limits offer greater financial stability and reduce the anxiety associated with the potential insolvency of their plans. Understanding these specific increases is vital for participants in these plans to accurately assess their retirement outlook.

Eligibility Criteria and Enrollment for PBGC Protections

While the new guarantees under the PBGC Update 2026 offer significant advantages, understanding the eligibility criteria and how enrollment works is paramount. The PBGC’s protections are not universal; they apply specifically to defined benefit pension plans sponsored by private-sector employers. Public sector pension plans, for instance, are not covered.

Enrollment in PBGC protection is automatic for eligible plans. Employers sponsoring defined benefit plans are required by law to pay premiums to the PBGC. This means that if you are a participant in a covered plan, you do not need to take any individual action to be protected. Your benefits are automatically insured up to the statutory limits, which have been enhanced by the 2026 updates.

What Constitutes a Covered Plan?

A plan is generally covered by the PBGC if it is a private-sector defined benefit pension plan. This includes both single-employer plans and multiemployer plans. However, there are certain exemptions. For example, plans maintained by professional service employers with 25 or fewer participants are generally exempt, as are church plans and certain plans for highly compensated employees.

- Private-sector defined benefit plans.

- Single-employer and multiemployer structures.

- Plans meeting specific ERISA requirements.

It is always advisable for individuals to confirm with their plan administrator whether their pension plan is indeed covered by the PBGC. This simple step can provide clarity and peace of mind regarding the security of their future retirement income.

When PBGC Steps In

The PBGC intervenes when a covered pension plan becomes financially unable to pay its promised benefits. For single-employer plans, this typically occurs when the sponsoring company goes out of business or terminates the plan. For multiemployer plans, intervention might happen when the plan is projected to become insolvent. Once the PBGC takes over, it becomes the trustee for the plan and begins paying benefits directly to retirees and future retirees, up to the guarantee limits.

The 2026 updates streamline some of these intervention processes, aiming for quicker and more efficient transitions for beneficiaries. This ensures that even in the event of a plan failure, there is minimal disruption to the payment of guaranteed benefits, reflecting the PBGC’s commitment to protecting retirees’ financial stability.

How the 2026 Updates Impact Your Retirement Planning

The PBGC Update 2026 holds significant implications for retirement planning, especially for those whose financial futures are tied to defined benefit pensions. These new guarantees provide a stronger foundation for planning, potentially reducing uncertainty and allowing for more confident long-term financial strategies. Understanding these impacts is crucial for individuals and financial advisors alike.

For many, particularly those in multiemployer plans, the increased guarantee levels mean that a larger portion of their expected pension is now secured. This can free up other retirement savings, allowing for investment in different assets or simply providing a greater sense of financial security. It shifts the risk profile for pension beneficiaries, making defined benefit plans a more reliable component of a diverse retirement portfolio.

Re-evaluating Your Retirement Strategy

With enhanced PBGC protections, it might be an opportune time to re-evaluate your overall retirement strategy. If your defined benefit pension was previously a source of concern due to potential underfunding or lower guarantee limits, the 2026 updates may alleviate some of those worries. This newfound security can influence decisions regarding other savings vehicles, such as 401(k)s, IRAs, and personal investments.

- Assess the protected portion of your pension.

- Adjust savings rates in other retirement accounts.

- Consider different investment strategies with reduced pension risk.

Consulting with a financial advisor is highly recommended to understand how these updates specifically apply to your individual circumstances. They can help you integrate your PBGC-protected pension into a holistic and optimized retirement plan.

Peace of Mind for Future Retirees

Beyond the financial calculations, the 2026 updates offer invaluable peace of mind. Knowing that your hard-earned pension benefits are better protected against unforeseen economic downturns or plan failures allows for greater confidence in your retirement years. This emotional security is a significant, albeit intangible, benefit of the strengthened PBGC guarantees.

The updates reinforce the idea that defined benefit pensions, while less common than in previous decades, still play a crucial role in providing stable retirement income. For those who have dedicated their careers to companies offering these plans, the PBGC’s commitment to their security is a welcome assurance, allowing them to look forward to retirement with greater optimism.

Navigating Potential Challenges and Future Outlook

While the PBGC Update 2026 brings considerable improvements, it is also important to acknowledge potential challenges and consider the future outlook for pension security. No system is entirely without its complexities, and staying informed about the PBGC’s long-term financial health and any further legislative changes is always a wise approach for beneficiaries.

One ongoing challenge involves the sustainability of the PBGC’s multiemployer program, even with the recent infusions of capital and increased guarantees. While the updates have provided a significant boost, the long-term solvency of some multiemployer plans remains a subject of careful monitoring. Similarly, economic fluctuations can always impact the financial health of single-employer plans and, by extension, the PBGC’s own financial standing.

Staying Informed About PBGC’s Health

The PBGC publishes annual reports and financial statements that provide insights into its fiscal health. For concerned beneficiaries, reviewing these reports can offer a clearer picture of the agency’s ability to meet its future obligations. While the 2026 updates have strengthened the PBGC’s financial position, especially for the multiemployer program, ongoing vigilance is key.

- Regularly check PBGC’s official website for updates.

- Review annual reports and financial statements.

- Understand the factors that influence PBGC’s solvency.

Staying informed allows individuals to anticipate potential changes and adjust their retirement planning accordingly. It empowers them to be proactive rather than reactive to developments within the pension landscape.

The Future of Defined Benefit Plans

The 2026 updates also prompt a broader discussion about the future of defined benefit plans in the U.S. economy. While these plans are less prevalent than in decades past, the PBGC’s strengthened role could encourage some employers to reconsider offering them, or at least provide greater stability for existing plans. The enhanced guarantees make defined benefit pensions a more attractive and reliable component of employee compensation.

Ultimately, the long-term outlook for defined benefit plans will depend on a combination of economic conditions, legislative support, and employer willingness. However, the 2026 PBGC updates undeniably contribute to a more secure environment for these crucial retirement vehicles, signaling a positive step forward for millions of American workers and retirees.

Practical Steps for Pension Beneficiaries in 2026

For individuals relying on defined benefit pensions, taking practical steps in light of the PBGC Update 2026 is essential. These actions can help you fully understand your protected benefits and ensure your retirement planning aligns with the new realities. Proactive engagement with your pension information is always beneficial.

The first step is to obtain your latest annual pension statement from your plan administrator. This document provides crucial details about your accrued benefits, vesting status, and beneficiary designations. Comparing this information with the new PBGC guarantee limits can give you a clearer picture of your protected income. Understanding the specifics of your plan is the foundation for effective retirement planning.

Contact Your Plan Administrator

Your plan administrator is your primary resource for specific information about your pension plan and how the PBGC updates affect you. They can clarify your covered benefits, explain any changes to your plan in response to the 2026 legislation, and confirm whether your plan is indeed covered by the PBGC.

- Request your latest pension benefit statement.

- Inquire about your plan’s PBGC coverage status.

- Ask about any plan-specific changes due to the 2026 updates.

Do not hesitate to ask questions. Clarity regarding your pension benefits is crucial for making informed decisions about your retirement. A well-informed beneficiary is a secure beneficiary.

Utilize PBGC Resources

The PBGC itself offers a wealth of information and resources on its official website. This includes detailed explanations of guarantee limits, publications for beneficiaries, and tools to help you understand your rights. Becoming familiar with these resources can empower you to stay abreast of any further developments and ensure you are maximizing your protected benefits.

The PBGC Update 2026 represents a significant positive development for pension beneficiaries. By taking these practical steps, you can fully leverage the enhanced protections and integrate them effectively into your overall retirement strategy, ensuring a more secure and predictable financial future.

| Key Aspect | Brief Description |

|---|---|

| New Guarantee Levels | Increased benefit protection for both single-employer and multiemployer plans, significantly boosting retirement security. |

|

|

| Multiemployer Boost | Most significant enhancements for multiemployer plans, providing a stronger safety net against insolvency. |

| Eligibility & Coverage | Applies to private-sector defined benefit plans; automatic enrollment for eligible plans, no individual action needed. |

| Retirement Planning Impact | Allows for more confident financial planning and potential reallocation of other retirement savings due to enhanced security. |

Frequently Asked Questions About PBGC 2026 Updates

The Pension Benefit Guaranty Corporation (PBGC) is a U.S. government agency that protects the retirement incomes of over 31 million American workers and retirees in private-sector defined benefit pension plans. It acts as an insurance program, stepping in to pay benefits up to certain limits if a covered pension plan fails.

The 2026 updates generally increase the maximum guaranteed benefit amounts, especially for multiemployer plans. This means a larger portion of your earned pension is now protected if your plan terminates. It enhances your retirement security without requiring any action on your part.

No, you do not need to do anything. If your pension plan is a private-sector defined benefit plan covered by the PBGC, your benefits are automatically insured. Employers pay premiums to the PBGC, establishing this protection for all eligible participants.

No, not all pension plans are covered. The PBGC primarily covers private-sector defined benefit plans. Public sector plans (state and local government), church plans, and certain small professional service plans are typically exempt from PBGC coverage.

You should contact your pension plan administrator for specific details about your plan and its PBGC coverage. Additionally, the official PBGC website (PBGC.gov) offers comprehensive information, publications, and tools to help beneficiaries understand their rights and protected benefits.

Conclusion

The PBGC Update 2026 marks a pivotal moment for pension beneficiaries. By taking these practical steps, you can fully leverage the enhanced protections and integrate them effectively into your overall retirement strategy, ensuring a more secure and predictable financial future.