2026 Healthcare Costs: Impact on US Retirement Planning

The escalating 2026 healthcare costs significantly challenge retirement planning in the United States, requiring proactive financial strategies to ensure future financial security and well-being.

As we look towards the future, understanding 2026 healthcare costs retirement planning implications in the United States becomes paramount. The landscape of retirement is continually evolving, and few factors exert as much influence on financial security as healthcare expenses. For millions of Americans, the dream of a comfortable retirement can quickly turn into a nightmare without adequate preparation for these significant and often unpredictable costs.

Understanding the Escalation of Healthcare Costs

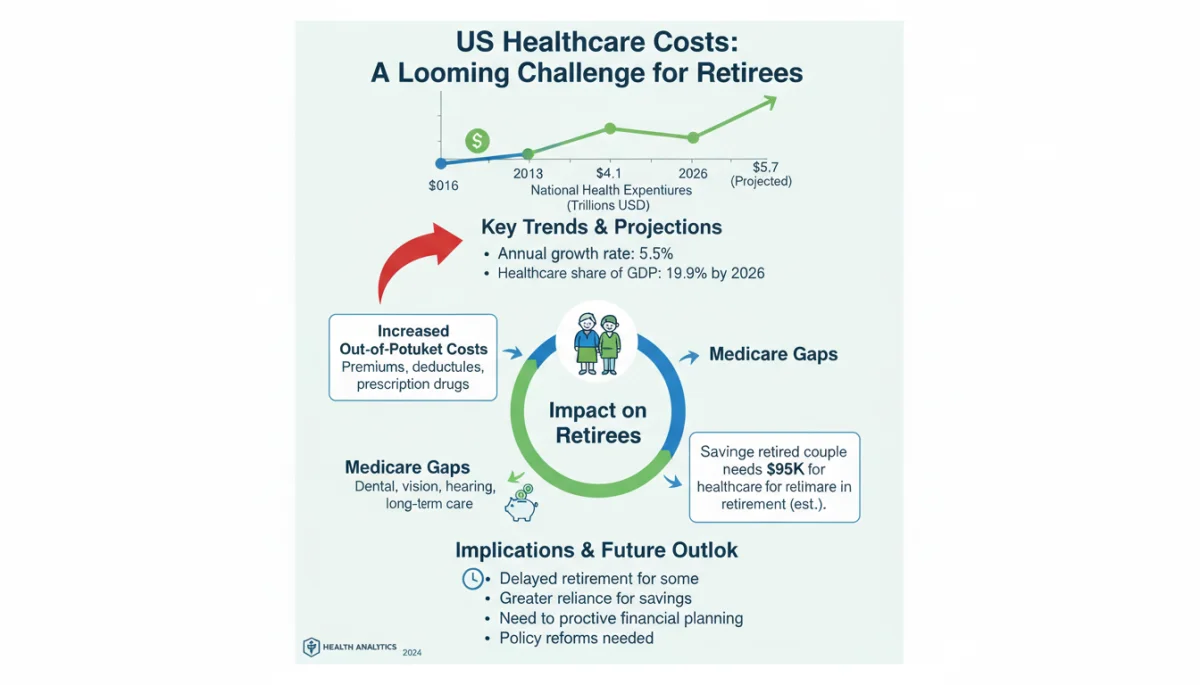

Healthcare costs in the United States have been on a relentless upward trajectory for decades, a trend that shows no signs of abating by 2026. This escalation is driven by a complex interplay of factors, from advances in medical technology and pharmaceuticals to the increasing prevalence of chronic diseases and an aging population. For retirees, this translates into a substantial financial burden that must be carefully considered in any long-term financial plan.

The sheer volume of medical services, coupled with the high cost of specialized care and prescription drugs, contributes significantly to these rising expenses. Without a clear understanding of these dynamics, individuals risk underestimating the funds required to maintain their health and quality of life in retirement.

Key Drivers of Healthcare Inflation

Several primary forces are pushing healthcare costs higher, directly impacting retirement savings. These drivers are interconnected and create a challenging environment for financial planning.

- Technological Advancements: While beneficial, new medical technologies and treatments often come with higher price tags.

- Pharmaceutical Costs: The development and marketing of new drugs, especially specialty medications, contribute significantly to overall healthcare spending.

- Aging Population: As the baby boomer generation enters and progresses through retirement, the demand for medical services increases, putting pressure on the healthcare system.

- Chronic Disease Prevalence: Lifestyle factors and longer lifespans mean more individuals are living with chronic conditions requiring ongoing, expensive care.

In essence, the rising cost of healthcare is not a temporary phenomenon. It is a structural issue within the U.S. system that requires retirees and pre-retirees to adopt sophisticated financial strategies. Understanding these drivers is the first step toward mitigating their impact on your retirement nest egg.

The Direct Financial Impact on Retirees

The financial impact of rising healthcare costs on retirees is profound and multifaceted. It’s not just about paying for doctor visits or prescriptions; it encompasses everything from insurance premiums and deductibles to out-of-pocket expenses for various services. Many retirees find that a significant portion of their fixed income is consumed by healthcare, leaving less for other essential needs and leisure activities.

Medicare, while a vital safety net, does not cover all healthcare expenses. Gaps in coverage, such as dental, vision, hearing, and long-term care, mean retirees often need supplemental insurance or substantial personal savings to cover these costs. The future of Medicare itself is also a subject of ongoing debate, adding another layer of uncertainty for those planning their retirement.

Medicare Gaps and Supplemental Coverage

Even with Medicare Parts A and B, retirees face considerable out-of-pocket expenses. These include deductibles, co-payments, and co-insurance. Many opt for Medicare Advantage plans (Part C) or Medigap policies to fill these gaps, which come with their own premiums.

Consider the average out-of-pocket costs for a healthy couple retiring at 65. Estimates suggest these costs could easily run into hundreds of thousands of dollars over their retirement years, even with Medicare. This figure can significantly increase if one or both individuals develop serious health conditions.

- Medicare Part A (Hospital Insurance): Covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care.

- Medicare Part B (Medical Insurance): Covers certain doctors’ services, outpatient care, medical supplies, and preventive services.

- Medicare Part D (Prescription Drug Coverage): Helps cover the cost of prescription drugs.

- Supplemental Options: Medicare Advantage plans (Part C) or Medigap policies provide additional coverage, but also incur additional premiums.

The challenge lies in accurately forecasting these costs, as healthcare needs can change dramatically over time. This uncertainty underscores the importance of a robust and flexible retirement plan that accounts for various healthcare scenarios.

Strategic Financial Planning for Healthcare in Retirement

Given the formidable challenge posed by escalating healthcare costs, strategic financial planning is no longer optional but essential for a secure retirement. This involves more than simply saving money; it requires a proactive approach to understanding potential expenses and utilizing available financial tools to mitigate risks. Starting early is crucial, as the power of compound interest can significantly boost savings over time.

Developing a comprehensive financial plan that specifically addresses healthcare needs involves several key components, from dedicated savings accounts to exploring various insurance options. It’s about building a robust financial fortress against unforeseen medical expenses.

Health Savings Accounts (HSAs) and Their Benefits

One of the most effective tools for saving for future healthcare costs is a Health Savings Account (HSA). Available to individuals with high-deductible health plans, HSAs offer a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

For those able to contribute to an HSA, it can serve as a powerful long-term savings vehicle. The funds can be invested and grow over decades, providing a substantial pool of money specifically earmarked for healthcare in retirement. Unlike Flexible Spending Accounts (FSAs), HSA funds roll over year to year, making them an ideal choice for long-term planning.

- Tax-Deductible Contributions: Reduces your taxable income.

- Tax-Free Growth: Investments within the HSA grow without being taxed.

- Tax-Free Withdrawals: Funds are tax-free when used for qualified medical expenses.

- Portability: HSAs are owned by the individual, not the employer, meaning they move with you.

Utilizing an HSA effectively requires foresight and discipline, but the financial benefits in retirement can be enormous. It’s a strategy that every pre-retiree should explore to help manage 2026 healthcare costs retirement.

The Role of Long-Term Care in Retirement Planning

Beyond acute medical needs, the prospect of needing long-term care represents one of the most significant and often overlooked financial risks in retirement. Long-term care, which includes assistance with daily activities like bathing, dressing, and eating, can be incredibly expensive and is generally not covered by Medicare. This can quickly deplete retirement savings if not adequately planned for.

The cost of nursing home care, assisted living facilities, or in-home care can range from tens of thousands to over a hundred thousand dollars per year, depending on the level of care and geographic location. Without a strategy to address these potential costs, retirees risk leaving their families with a substantial financial burden or compromising their own financial independence.

Options for Long-Term Care Coverage

There are several avenues to consider when planning for long-term care. Each option comes with its own set of advantages and disadvantages, and the best choice often depends on an individual’s financial situation, health status, and personal preferences.

Traditional long-term care insurance policies are designed to cover these specific costs. However, premiums can be substantial and have risen in recent years. Hybrid policies, which combine life insurance or annuities with long-term care benefits, offer another alternative, providing a death benefit if long-term care is not needed.

- Traditional Long-Term Care Insurance: Provides coverage for a specified period or amount once certain triggers are met.

- Hybrid Life Insurance/Long-Term Care Policies: Combines a death benefit with the option to access funds for long-term care.

- Self-Funding: Relying on personal savings and investments to cover potential long-term care costs.

- Medicaid: A safety net for those who have exhausted their financial resources, though it often involves strict eligibility requirements.

The decision to purchase long-term care insurance or to self-fund requires careful consideration and often consultation with a financial advisor. Proactive planning in this area is critical to protect your retirement savings from potentially catastrophic expenses.

Navigating Future Healthcare Policy Changes

The healthcare landscape in the United States is continuously subject to policy changes, which can significantly alter the financial burden on retirees. Understanding potential legislative shifts and their implications is crucial for adapting retirement plans. While predicting the future of healthcare policy is challenging, staying informed about ongoing debates and proposals can help individuals make more resilient financial decisions.

Potential changes to Medicare, the Affordable Care Act (ACA), and other healthcare programs could impact everything from premium costs to covered services and out-of-pocket maximums. Retirees must remain agile and prepared to adjust their strategies as the policy environment evolves.

Anticipating Legislative Developments

The political climate often influences healthcare policy, with discussions frequently revolving around affordability, access, and the sustainability of existing programs. Monitoring these discussions and understanding the potential outcomes can help retirees and pre-retirees anticipate future financial impacts.

For instance, proposals to lower prescription drug costs or expand Medicare benefits could alleviate some financial pressure, while reforms that increase beneficiary contributions could lead to higher out-of-pocket expenses. Staying engaged with reliable news sources and consulting with financial professionals who specialize in retirement planning can provide valuable insights.

- Medicare Reforms: Potential changes to eligibility, benefits, or funding mechanisms.

- Affordable Care Act (ACA) Adjustments: Modifications that could affect insurance markets and subsidies.

- Prescription Drug Pricing: Ongoing efforts to control the cost of medications.

- State-Level Initiatives: Local policies that might impact healthcare access and costs.

Ultimately, a flexible retirement plan that can adapt to policy changes is more likely to withstand the uncertainties of the future. This adaptability is key to managing the complexities of 2026 healthcare costs retirement planning.

Empowering Your Retirement with Proactive Healthcare Planning

Empowering yourself for a fulfilling retirement in the face of rising healthcare costs requires a proactive and informed approach. It’s not enough to simply hope for the best; active engagement in your financial planning process, particularly concerning health expenses, is essential. This involves not only saving diligently but also making informed decisions about insurance, investments, and lifestyle choices.

The goal is to build a retirement fund that is resilient enough to cover both expected and unexpected healthcare needs, allowing you to enjoy your golden years with peace of mind. By taking control of your healthcare planning, you can significantly reduce financial stress and enhance your overall well-being in retirement.

Practical Steps for a Secure Future

Taking concrete steps today can make a significant difference in your financial security tomorrow. These steps should be integrated into your broader retirement strategy and reviewed regularly to ensure they remain aligned with your goals and the evolving healthcare landscape.

Consider consulting with a fee-only financial advisor who specializes in retirement planning. They can help you assess your current situation, project future healthcare costs, and develop a personalized strategy that incorporates various financial tools and insurance options. Additionally, maintaining a healthy lifestyle can reduce the likelihood of costly medical interventions, further safeguarding your savings.

- Start Saving Early: The earlier you begin, the more time your investments have to grow.

- Utilize HSAs: Maximize contributions to Health Savings Accounts if eligible.

- Explore Long-Term Care Options: Research and decide on the best approach for potential long-term care needs.

- Stay Healthy: Lifestyle choices can significantly impact future healthcare expenses.

- Review and Adjust: Regularly revisit your retirement plan to account for changes in health, finances, and policy.

By embracing these strategies, individuals can transform the challenge of 2026 healthcare costs retirement planning into an opportunity for greater financial security and a more enjoyable retirement.

| Key Aspect | Brief Description |

|---|---|

| Rising Costs | Healthcare expenses in the U.S. are continually increasing due to technology, drugs, and an aging population. |

| Medicare Gaps | Medicare does not cover all expenses, necessitating supplemental insurance or substantial personal savings. |

| HSAs & Long-Term Care | Health Savings Accounts offer tax benefits, while long-term care insurance addresses significant future care costs. |

| Policy Changes | Healthcare policies are dynamic; staying informed and adapting plans is crucial for financial resilience. |

Frequently asked questions about healthcare costs and retirement

The main concern is the continuous escalation of healthcare expenses, which can significantly deplete retirement savings. This includes rising premiums, deductibles, and out-of-pocket costs for services not fully covered by Medicare, impacting financial security and quality of life in retirement.

An HSA offers a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. This makes it an excellent long-term savings vehicle specifically designed to cover healthcare costs in retirement, including those not covered by Medicare.

No, Medicare does not cover all healthcare expenses. It has deductibles, co-payments, and does not typically cover services like dental, vision, hearing aids, or most long-term care. Retirees often need supplemental insurance or personal savings to bridge these significant coverage gaps.

Long-term care, encompassing assistance with daily living activities, is extremely expensive and generally not covered by Medicare. Without proper planning, such as long-term care insurance or dedicated savings, these costs can quickly exhaust retirement funds, creating a major financial burden.

Changes in healthcare policy, including reforms to Medicare or the ACA, can impact costs, coverage, and access to services. Retirees must stay informed and maintain a flexible financial plan to adapt to legislative shifts, ensuring their healthcare funding remains robust.

Conclusion

The challenge of 2026 healthcare costs retirement planning in the United States is undeniable, demanding careful consideration and proactive strategies from every individual approaching or already in their golden years. By understanding the drivers of rising expenses, leveraging financial tools like HSAs, planning for long-term care, and staying informed about policy changes, retirees can build a more secure and resilient financial future. The path to a comfortable retirement is paved with diligent preparation, ensuring that healthcare needs are met without compromising overall financial well-being.